Target-date funds have become a mainstay of workplace group retirement plans across Canada in recent years. Sun Life, the country’s top provider in the segment reports that close to 68% of its capital accumulation plan sponsors have chosen a target-date fund as their default investment option. Prior to that, it was common in the industry to deposit the assets of members who did not make an investment selection into a balanced fund.

“Target date funds have proven to be an ideal solution for many of our capital accumulation plans,” said Alexandra Barbu, assistant vice-president, investment solutions & group retirement services at Sun Life Canada. “Over 80% of our plan members invest in them.”

According to Sway Research, target-date fund assets totalled a staggering US$3.47 trillion in 2023, making them a cornerstone of American workplace retirement plans like 401(k)s. Lineups from investment giants such as Vanguard, Fidelity Investments and BlackRock dominate this space.

It’s been a different story in the Canadian ETF category.

In April 2023, Evermore Capital Inc. terminated its Evermore Retirement ETFs, just a year after their debut. The move marked the end of Canada’s first lineup of target-date ETFs. Was it a temporary setback? Or does the failed launch reflect long-term barriers to the adoption of target-date ETF funds in the Canadian market?

How target-date funds work

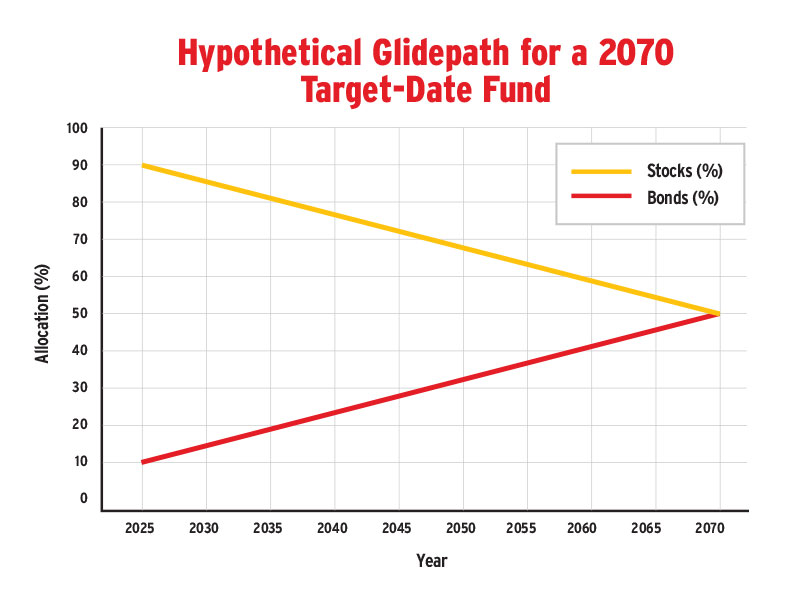

The appeal of target-date funds lies in their simplicity. While their composition may vary, all target-date funds share a common feature: the “glidepath.” This concept refers to an asset allocation strategy that primarily considers an investor’s time horizon to determine the mix of securities.

For example, a 2070 target-date fund, intended for someone retiring around that year, might start with an allocation of 90% equities and 10% fixed income. The reasoning is straightforward — longer time horizons generally allow for greater risk tolerance, so the portfolio prioritizes growth.

In contrast, a 2030 target-date fund, intended for someone retiring sooner, might currently allocate 40% to fixed income and 60% to equities. With a shorter time horizon, risk tolerance decreases, and the portfolio focuses more on capital preservation and income rather than aggressive growth.

Crucially, target-date funds differ from the asset allocation ETFs popular among investors in Canada. Unlike static holdings, these funds evolve over time. The glidepath ensures that as investors age and approach retirement, the portfolio adapts to their shortening time horizon.

By 2050, that 2070 target-date fund won’t consist of 90% equities and 10% fixed income. It will have shifted gradually towards a more conservative allocation, increasing exposure to fixed income.

Similarly, the 2030 target-date fund wasn’t always bond-heavy — a decade ago, it would have held a significantly higher allocation to equities. This dynamic adjustment is what sets target-date funds apart.

Capital gains efficiency

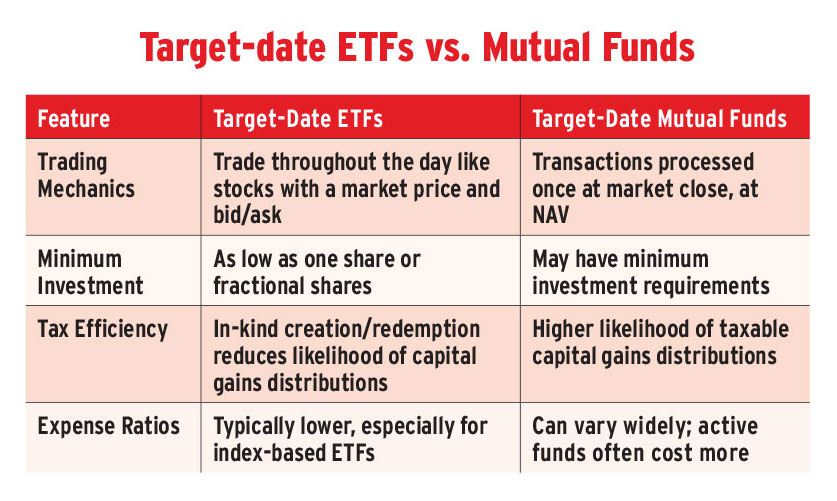

Target-date ETFs follow the same asset allocation strategy as their mutual fund counterparts, but leverage a different fund structure. This reduces capital gains distributions.

Mutual funds, especially actively managed ones with high turnover, can be inefficient when it comes to capital gains distributions. These occur when funds sell appreciated securities to meet investor redemptions, passing the tax burden to remaining shareholders.

In contrast, ETFs mitigate this issue through a creation-and-redemption mechanism. This process involves ETF issuers working with authorized participants to exchange blocks of ETF shares, called creation units, for underlying securities.

The mechanism provides liquidity while keeping the ETF’s market price aligned with its net asset value (NAV) by meeting supply and demand.

In Canada, the creation-and-redemption process is classified as an in-kind transaction, meaning it does not trigger a taxable event. For advisors managing taxable accounts, this difference can result in considerable tax savings compared to mutual funds.

BlackRock or bust

Almost two years after the Evermore Retirement ETF line was withdrawn, the only target-date ETFs available in Canada are offered by BlackRock iShares (IDTF). The global giant offers a lineup of 10 target-date ETFs, staggered in five-year increments. They’re traded in U.S. dollars, and offer a 0.11% expense ratio.

Asset allocation is executed using an ETF of ETFs strategy, where ITDF holds other passive index-tracking iShares ETFs designed to replicate the 2050 Target Date Custom Benchmark.

For ITDF, the portfolio includes allocations to U.S. large-cap blend, international developed and emerging market large-cap blend, U.S. small-cap blend, U.S. REITs, long-term treasury bonds and intermediate corporate bonds.

While Canadians don’t differentiate between short- and long-term capital gains like U.S. investors, what’s key is the absence of capital gains distributions, which is universally beneficial when holding these ETFs in non-registered accounts.

Barriers to adoption in Canada

The first and most obvious objection many advisors have is that target-date ETFs simplify asset allocation too drastically. These funds rely on a single variable — time horizon — to determine the strategy.

While effective for simplicity, this one-size-fits-all approach may not account for other critical factors such as client risk tolerance, goals or changing market conditions.

Another concern is the allocation strategy itself, particularly considering positive stock-bond correlations, which have persisted since 2022.

The BlackRock LifePath ETFs, for example, limit their allocations to equities and fixed income, with no exposure to alternative assets such as commodities, managed futures, private equity or real estate (outside of REITs). This lack of diversification may leave portfolios vulnerable.

The most vexing barrier for Canadian advisors is the double challenge of withholding tax and currency risk.

First, because these ETFs are U.S.-domiciled, 15% of distributions are withheld for taxes unless they are held in an RRSP. That is the only registered account exempt from this levy under tax treaties.

Moreover, these ETFs are subject to currency risk. With the greenback at historic highs against the Canadian dollar, advisors opting to use them face the burden of a weaker loonie and currency conversion costs.

Another factor that Canadian advisors and investors might find unappealing about the iShares LifePath target date ETFs is their lack of Canadian investment exposure.

Research from Vanguard suggests that up to a 30% overweight in Canadian equities can provide several advantages, including lower portfolio volatility, reduced currency risk and better tax efficiency due to the preferential treatment of eligible Canadian dividends in taxable accounts.

However, as U.S.-based products, the iShares LifePath ETFs do not incorporate this home-country tilt. Advisors relying on these ETFs would need to supplement Canadian equity exposure with a separate fund, effectively defeating the purpose of having a turnkey solution for clients.

The future’s so meh

As it stands, it’s unlikely that U.S. target-date ETFs will gain significant traction with Canadian investors. Even in their home market, the reception among U.S. investors and advisors has been lukewarm.

ITDF, launched in October 2023, has only amassed $21 million in AUM — far below the $50 million threshold typically needed for financial viability.

If these target-date ETFs are struggling to gain traction with the sizable U.S. advisor population, it’s reasonable to assume they won’t fare much better in Canada.

That said, long-term tailwinds could eventually propel these products to greater adoption. The continued growth of the domestic ETF industry, combined with an aging population increasingly looking for simple, automated solutions, presents an opportunity for target date ETFs down the road.

As it stands, the most appropriate use-case for these ETFs in Canada is limited to younger clients with smaller portfolios and U.S. dollars seeking a low-cost, hands-off solution. That’s a pretty slim target.

Click image for full-size chart

Click image for full-size chart

This article appears in the February issue of Investment Executive. Subscribe to the print edition, read the digital edition or read the articles online.